What Happens If House Prices Go Down?

One of the key concepts behind how a reverse mortgage works is that your home will increase in value over time – helping to offset the interest that accumulates on the loan.

But what if that doesn’t happen?

What if house prices don’t go up… or worse, what if they go down?

This is something I’ve covered before in broader terms (see my article and video on What If There’s a Housing Market Crash), but today I want to look at it in the context of the current Canadian market – where house prices are actually down year-over-year.

And I’m going to show you a bit more detail to put your mind at ease when it comes to house prices.

This isn’t just something that relates to reverse mortgages but owning real estate and owning a home in general – so if you know anyone who is worried about house prices right now, feel free to share this article with them.

As always, you can read the full article below or watch the video version:

First, What Is A Reverse Mortgage?

Before I get to the detail – if you’re looking at reverse mortgages and new to them as a concept, the best place to start is with my free reverse mortgage guide.

It will give you all the information you need to know on reverse mortgages in Canada.

What Happens When House Prices Go Down?

House price appreciation is an important part of how you protect your home equity with a reverse mortgage (or any other mortgage).

Since you continue to 100% fully own your home, you get to keep 100% of the increase in value – even if you’ve borrowed 10%, 40%, or even 55% of the original value.

But if prices are falling, like they are almost across Canada right now at the time of writing (August 2025), people understandably get concerned.

They see the reverse mortgage interest accumulating but don’t see the home value rising to offset it.

It’s a valid worry, so let’s explore it.

House Price Growth & Interest

Let’s look at a simple example:

- Your home is worth $800,000.

- You take out a reverse mortgage for $200,000 at 6.5% interest.

Now imagine your home grows in value at an average of 5% per year.

That’s $40,000 in growth in the first year alone – compared to $13,000 in interest on the reverse mortgage.

That means your net equity still increased – by $27,000 in just the first year alone – even after accounting for the reverse mortgage interest.

This is why 99% of Canadians who have taken out a reverse mortgage have equity remaining when it is paid off.

When home prices rise at a normal rate, your equity doesn’t shrink – it actually grows for many folks who have a reverse mortgage.

But Wait – Aren’t House Prices Going Down Just Now?

Right now, yes – they are.

House prices have dropped across most of Canada over the past couple of years – at the time of writing this article (August 2025).

That’s led many people to worry that the interest from a reverse mortgage will start eating away at their equity, and quickly.

And if you only look at the short term, it can absolutely feel that way.

But that’s not how real estate works over the long run.

House Prices & Home Value Growth

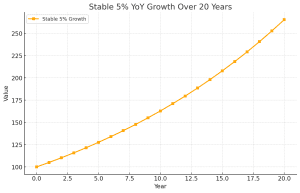

A lot of people hear something like “house prices go up 5% per year” and assume that means they go up exactly 5% every year like clockwork.

You might think it looks something like this:

That’s not how the real world works.

It is not a straight line upwards. That’s not how an average rate works.

There are always going to be periods of above-average growth and below-average growth – including years where prices go down – the average rate being what you get when you even them all out.

The key is to zoom out and look at the bigger picture – which is what you need to do when considering the average home value growth rate.

House Prices – The Reality

When you actually look at how home prices behave over time, you’ll find that they don’t grow in a straight line, like the chart above.

In fact, even in a scenario where prices average 5% growth per year over 20 years, you’ll still see multiple years where prices go down.

Here’s an example of what 5% home value growth over 20 years really looks like (including the line from the previous chart):

If you look at the chart above, 6 of the 20 years saw prices go down – including a 10% drop one year and even three consecutive down years.

But despite all of that, the long-term average still worked out to 5% growth over 20 years.

That’s the nature of real estate.

That’s the nature of investing in any market in anything (stocks, art, cars etc) – prices will go up and prices will go down – you look to make profit in the long-term based on the expected average growth rate over that period.

Not only that, but the lenders are actually banking on your home going up in value – or they simply wouldn’t lend you the money (or at least as much of it) – see my article on What’s The Catch With A Reverse Mortgage for a more detailed discussion of this concept.

House Prices In Canada

Let’s go beyond theoretical examples and look at real numbers in Canada.

-

From 2005 to 2025 (20 years), Canadian home prices rose by an average of 5.57% per year – despite prices having fallen so far in 2025.

-

From 1995 to 2015 (20 years): 5.41%.

-

From 1985 to 2005 (20 years): 5.82%.

-

From 1975 to 1995 (20 years): 5.74%.

No matter how you slice it, the story is the same: over 20-year periods, Canadian real estate has consistently returned just over 5% annual growth.

(The above numbers were calculated using the BIS Selected Residential Property Price Index for Canada which goes back to 1970. Finding accurate housing market data for Canada is very difficult but no matter your source you’ll get the same conclusion: prices rise between 4% and 6% in the long-run)

Down Years & Up Years

Now, does that mean it’s all smooth sailing?

Definitely not.

Since 1975 (in the last 50 years), there have been over a dozen individual years where prices went down.

That means that more than 20% of the time in the past 50 years, house prices went down.

Some of those drops were substantial.

Yet that period still average 5% growth over the entire period, on average.

If you pan out and hold your home over the long run, history shows that those temporary drops get smoothed out – and average growth takes over.

If you had panicked and sold during a down year, you’d have missed out on the gains that followed.

That’s the cost of thinking short-term when it comes to something that is a long-term investment, like your home.

Thinking Long-Term

House prices will go up – and they’ll go down.

Sometimes the swings will be small. Sometimes they’ll be dramatic (both up and down – we’re seen both sides of this in just the last 5-6 years).

But over time, the trend has been remarkably consistent.

If you’re taking out a reverse mortgage (or almost any mortgage really), you should not be looking for a one-year or two-year play.

Reverse mortgages aren’t well designed or suited for short-term purposes, they’re designed to let you live in your home forever, while taking equity out of it.

If you do use a reverse mortgage for a short-term loan, you can do so – but know that you are taking on additional risk as you’ll be subject to the short-term fluctuations that can be seen in the housing market. (For more on this, see my article The Biggest Mistake You Can Make With A Reverse Mortgage)

My recommendation with a reverse mortgage is to approach it from the perspective that you’re using your home equity as part of a long-term retirement strategy.

That means you should ignore the short-term noise – just like you would with long-term investing.

Sit back and enjoy the 5% year over year growth – you can do that and completely ignore the ‘real’ house prices changes that are occurring, knowing that they are just short-term noise.

Whether it’s a bubble or a boom, prices have always averaged out to somewhere between 4% and 6% annual growth in Canada when measured over a decade or more.

Summary – What Happens When House Prices Go Down?

House prices are down right now and they are going to do down again at some point in future (that is almost an absolute certainty).

It’s completely fair to feel uneasy when the news is full of doom and gloom about house prices – especially in today’s 24/7 news cycle where bad news is repeated multiple times a day, every day, for weeks on end.

But the reality is that the Canadian housing market has always bounced back – and consistently delivered average annual growth in the 4% to 6% range, when viewed in the long-term.

This is the correct perspective you need to take for a reverse mortgage (or any mortgage) – as these are intended to be long-term tools. And your home is considering a long-term asset.

You don’t need home prices to go up every year (that is simply not going to happen, ever) – they just need to go up over time.

And history has shown that, in Canada, they do.

Get A Free Professional Reverse Mortgage Assessment In 90 Seconds

If you’re wondering whether a reverse mortgage might be the right solution for your needs, I offer a free professional assessment to help you figure that out.

I’ll let you know if a reverse mortgage is a good fit – or if there’s a better alternative for your situation.

I’ll show you a comparison table of the lenders and all your options – including all the hidden costs & fees in each option – so you can make an educated and informed decision.

The assessment only takes 90 seconds and is completely obligation-free.

All it takes is 90 seconds – click here to get started.

A Canadian Chartered Accountant and licensed Mortgage Professional – creator of Reverse Mortgage Pros – the #1 reverse mortgage specialists in Canada. I make it my mission to educate Canadians about how reverse mortgages work so that you can make an informed and educated decision that’s right for you and your family.